Last month, a top financial industry regulator voiced concerns that banking and FinTech collaborations might be “blurring the lines” between banking and commerce.

According to Michael Hsu, CEO of the Office of the Comptroller of the Currency (OCC), such “blurring” can undermine public confidence in the financial services industry, just as it did in the months leading up to the 2008 global financial meltdown.

No one is disputing Hsu’s insistence that public faith in the financial services industry is essential, but recent data shows Americans’ confidence in the U.S. banking industry hasn’t wavered significantly in the last two years — despite three high-profile bank failures in 2023.

In fact, additional research confirms most U.S. consumers value the speed and efficiencies being nurtured through bank/FinTech alliances.

A recent PYMNTS Intelligence study, “How Open Banking Can Provide Fast and Easy Consumer Payouts,” produced in collaboration with Trustly, shows most consumers believe the byproducts of open banking — the legal framework fostering bank/FinTechs partnerships — are beneficial.

That’s because many banks still rely on legacy technology to support customer products, and much of that technology cannot support the sort of user experience today’s digitally-savvy consumers have come to expect.

Instead of being housed in closed legacy banking platforms, open banking permits financial institutions to share customer data with FinTechs, enabling the two entities to create modern application programming interfaces (APIs) that can enable an accelerated transfer of funds between banks, consumers and merchants.

“How Open Banking Can Provide Fast and Easy Consumer Payouts” found that most consumers seem to appreciate this transformation. A significant segment of the nearly 2,600 consumers surveyed for the report said they prefer the faster payments that open banking is helping to foster.

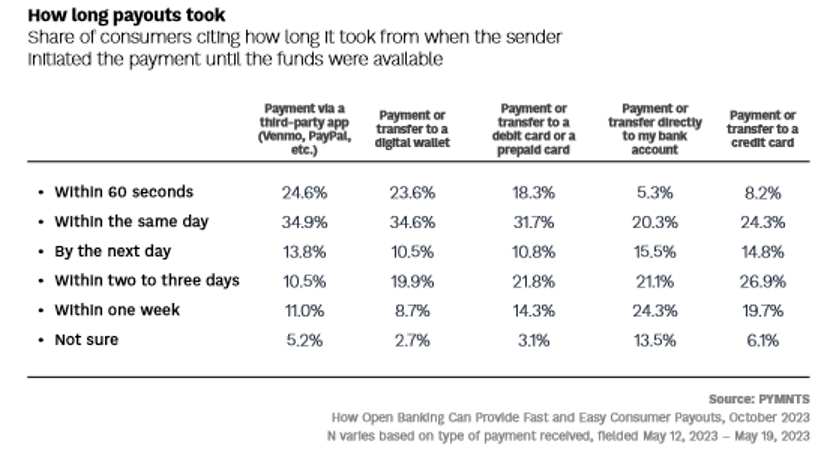

Most respondents said they expect payments processing to be completed in a timely fashion. Yet, 45% said the current payments process their banks offer can take up to seven days to complete, a turnaround that 4 in 10 consumers said is “unsatisfactory.”

Now consider the 5% who are able to complete bank transactions within 60 seconds: 92% of them said such velocity was “extremely” satisfying.

The fact that just 5% of these bank payouts can be completed in about a minute indicates only a small fraction of consumers can now experience instant payments. This suggests the banking industry still has work to do if it hopes to deliver on customer expectations.

The survey finding also suggests consumer confidence isn’t eroding in the face of bank/FinTech collaboration. Just the opposite, in fact.

Younger consumers and frequent receivers both said they are comfortable connecting payouts directly to their bank accounts through an open banking arrangement if it means faster transactions. And 50% of millennials said they would be “extremely influenced by the availability of open banking connectivity” when they select merchants and providers in the future.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More